Pension in Israel - learn responsibility

January 23, 2017

Take care of the retirement by Spring, and a dream dress! Without difficult not to pull out and pension from the pond! Under the lying stone and the pension does not flow! Sit, old and young, but listen - Pension in Israel!

Disclaimer. This article is solely reference and in no way an indication of any actions. I am not responsible for your operations with your pensions, and all changes in the current state of affairs are on your own risk. The professional council should apply to a proven pension consultant. No retirement consultant this article advertises.

Why such an ominous disclaimer? The fact is that while we are young and capable, everything can be fixed. It is a shame, but errors with the purchase of a car or a loan takes. Seriously beat the mistake in life with the purchase of an apartment, but they can be overcome. The pension accounts for the age when the capacity and activity decrease on the exhibitor, and the complexity of the correction of errors in ensuring old-age and the size of pensions on the exponent increases.

I reveal this topic as I understood it after communicating with retirement consultants and visits to seminars. Who is it intended? Oddly enough, not only completely adults and elderly, but people of all ages. It works so much that the sooner it is to get, the better the result will be the result. But before any actions, a million times recheck this and any other information.

The topic is borne, the article is planned for decent sizes, but I will try ignorly, with prefers and curtains. In addition, you have the opportunity to read theory for free, I paid for this information both money and considerable number of my time. I do not think that I can ask to pay something to me, but anyone who wishing to thank the personal initiative will find at the end of the article a block with information, how to give a "cup of coffee" and help the project. Go.

Why is there no pensions in Israel?

The problem is that since 2013, the pension in Israel is not observed. But since I always write on the Hollywood scenario, you, of course, you understand that the main character to shoot at the very beginning of the film can not. Maximum - shoot into soft fabrics. So where are you shot? To understand this, it will take a small theoretical and historical excursion.

The first in history to retirement was thought of the French military during the Great French Revolution. In the free translation, they came to the new revolutionary government and said: "We were fought, the king was dropped, they took Bastilia, the belly did not spare. Throw us on Chardonnone and Cigarettes in Older. " It was a few centuries ago, and since then in different countries in one way or another power and people thought about the fact that old people need to live on something.

In Israel, before that, of course, they thought too. Until the 70s, approximately 70% of Israelis worked in the public sector. They were due to the state pension, which was called "Pensions Tankivit" ("Tatziv" - budget). It covered from the experience and was calculated as follows: for each year, 2% of the salary was assumed. The maximum percentage of the pension was 70% of the salary (which is equivalent to 35 years old). In other words, if my salary was equal to 10,000 shekels, then the pension would be 7,000. Such a tankivit pension in some industries continued to exist until 2013.

In the 70s, the "bourgeois revolution" occurred, and collective agreements appeared. Now the employer was supposed to deduct a certain part in the accumulative funds, of which the pension was formed. These funds are called "Gemel Coupling." Money transferred there onlyemployer; The worker did not list anything and with a dreamy appearance represented how at the age of 70 he will go to the world journey through Israel. Upon reaching the retirement age, the employee received all the money at once.

In 2008, there were two significant points. Many will immediately think that the crisis. He, of course, happened, but just so coincided. So in 2008, specially trained people considered that the young people who arrived in the 60s in the 60s inexorably moves to the autumn of the century released by him, and this retirement should be paid. And where? There is no money, as always, no. As such as the pace by 2026, the crawling of the caterpillar of Israel will open, undergo wonderful metamorphosis and will turn in butterfly bankrupt. And all residents will remain beautifully touching the sunset.

The second point is not less beautiful. Because the pension fell into account of the Unified amount, then imagine that it began to occur. A person who received 100,000 shekels all his life comes to the bank and discovers Jack Pope in the amount of 2.000.000. Such a person occupied an average of six months to two years to lose to the preference and lose all two million. When the last curtisank was escaped from him, he walked in the Bituah Leumi. And everyone became very sad: a pensioner, because he had to knock himself a guide to ensuring a subsistence minimum, and unuse and aunts from Bituah Leumi, because the villa in the caisary herself will not build herself, and here they go all sorts.

Until the thunder, reforms were held: the GEMELLE'S COMMUNICATION The money starts to list not only employers, but also workers, and the pensions themselves are listed by the addressees not one piece, but payments. The state pensions were canceled. The latter came to them in 2013, army (I can be wrong about historical facts, correct if you know more precisely).

So, the state pension in Israel is absent. And what is present?

How is the pension in Israel formed?

First source - Bituah Leumi. This is a state insurance company. And the retirement age is an insured event. If you, like me, a man, and you will seem to live to 67 years, then 1531 Shekel is your cookie on a happy old age. If you are a woman, then cookies you will get in 64. Do not make fire to numbers, there are those who are still retired in 62, and now they are already actively thinking about even greater increase in retirement age, for we live too long.

Why is this not a pension? Because it is an old-age allowance (Zikna's kitsvath), and how can the language turn 1531 Shekel to call a pension? But not everything, of course, is so simple. To get this oil to bread, you need to perform a condition. Have a minimum experience. Or 60 months Over the past 10 years. Or 144 months For all the time staying in Israel. For those who arrived in Israel already in pre-expensive / retirement age, there is Ziwent's kitswat (Muchhedet - special). It does not require experience, but there is a lot of restrictions.

In addition, for each year excess 9 years(since 2017; it used to be over 10 years old) you can receive 2% bonus and increase 1531 Shekel to maximum 2250 Shekels(that is, 50% of the amount).

Lifehak.In order for no problems with the Luum bitahs, their salary sheets (Tlushi masked) and 106 forms are desirable to store until retirement. Of course, your relationship with employers for Leumi bituahs are usually transparent and stored in them in databases. But if suddenly something happens to their bases at the time of their retirement, then to prove someone something without salary sheets and 106 forms will be categorically difficult. Therefore, print the leaves, put in a file, a file in an egg, an egg in the duck, duck into the hare, and so on ...

So, at the moment we have with good scenario 2250 Shekels who should brighten up our nostalgia on youth. But they can be increased. The state is interested in not to give them, says: "An old man, and do not take this money! If you take, then on every shekel, earned over 5000 per month, we will cut your benefit. That is, if you have a salary of 7,500 per month, then you will deprive the benefits at all, argue? " And we, even even old, but not yet in Dementia, we answer: "We, of course, did not finish the gymnasis, but so far I have a hrenovo. What is our benefit? " What the state, shouting and rubbing and rubbing the cold bony hands, is responsible: "If you do not take this money to 70 and you will not play the box along the way, then for each year the deferment you get another 5% bonus from this amount."

Moreover, 70 years in general, a very important date in the life of every citizen of Israel. And not because you can see that you have lived before these years. Although I would be very pleased. And because at that age it becomes no matter how much you earn to get this allowance (although, for some reason, it seems to me that at this age there is already much no matter). For example, in 2015, the Director-General of the Leumi Bank for a month approximately received 675 thousand shekels, if you believe the outgoed information. So if she had 70 years old, she would have calmly went to the Bituah Leuma and asked for a 2250 shekels to throw her (plus 5% of the bonus for each year she did not take this money) to his pocket expenses. We wish the director for many years of life and move on.

This money will be paid to you, even if you live in another country. With the reservation that the country of social deductions should be concluded with this country of Israel. That is, if at old age, you wanted to be closer to grandchildren and beat the children who live in Canada with their marators, there are no problems. Catch up to Canada and get your legitimate 2250.

With this part sorted out. Bituah Leuma pays us an insured event.

second origin - These are deductions. The very deductions, which since 2008, the Ministry of Finance obliged us to do.

For 2017, these deductions account for 6.5% of the salary from the employer and 6% by the employee. This is called "Tagmulim". And here are another 6%, expelled by the employer who are called "Pitsim" - money for dismissal.

By the way, there is the following rule: if you dismiss yourself, then you get this money in such a proportion, and if the employer fits you, then it is obliged to pay 2.33% for each month from the moment of work. But here the employer has tools to relieve themselves. For example, it can pay interest not with 100% of your salary, which includes salary itself, additional hours, trips, premiums and other tastes, and from 70%. It all depends on your contract with the employer, so trading, ask, emphasize the attention, "and compote?"

This money can be deducted in the following funds: either Keren pension, or "Kupate Gemel" or "Bituah Menaelim".

What is the difference?

First of all, Kupaat Hemel and Keren pension are group contracts. The advantages are that always below the mining percentage than in individual contracts. Cons - Conditions provided for some time lapse and can always be changed.

Bituah Menaelim is a personal contract. Minus - a high percentage of service. Plus - the conditions provided to iron are preserved before terminating the contract. The deductions in Bituha Menaelim make up 5% of the employee, 5 from the employer and 8.33% - Pisuim. From 2013, Bituah Menaelim is a very unfavorable tool for accumulating pensions.

We will make a tablet for clarity (interest interests are the deductions of the employee + the deductions of the employer + maximum pisuim):

It becomes clear from the plate that Menalem's bituah is now not profitable at all, but insert the remark below.

Mekadem.

There is such a concept - Mekad. In other words, the divider. When you have achieved a retirement age, and you, let's say, a million pension deductions have accumulated, they will be paid to you by payments. What payments? Who and how did you decide how the pension is paid in Israel? For this purpose it is used by Mekada - the coefficient for which all the deductions will be done and the resulting amount will begin to pay monthly. Mekadem depends on the average life expectancy. Today, boys are 78 years old, and girls 85. The insurance company counts and pays. If this world left earlier than your pension savings ended, heirs will receive them. If later, payments are not stopped, the insurance continues to pay. Therefore, insurance is counting on a divider so as to pay you for your accumulation and not start paying from your pocket. Today, Mekada is approximately equal to 240. Some time ago it was less than 200. Even before - 180.

That's it then, Bituah Menaelim was very profitable. Since this is an individual contract, then Items remains fixed for you, and you knew exactly what amounts you get on pensions. Exactly on January 1, 2013, insurance companies realized that the holders of the Menaelim's Bituahs are very curlyingly with such a fixed mekadem, and covered the shop.

Dmy Niul

There are two types of them:

- dMY NUUL MI AVKAD(commissions with enumerations)

Keren pension a maximum of 6%. This percentage is taken out of the deductions. - dmy Nouli Hisachon(Commission with savings)

Keren pension a maximum of 0.5%. This percentage is taken from all savings constantly, every year.

What to do with these percentages? Reduce. Trade with the insurance agent, like Berserk, beat as gladiator. What is most importantly reduced? Intuition suggests that 6%, but the question is trimmed, so we, quickly oriented, responding that 0.5%, and we are right. Why? Obviously, because we do not want with the money for which the Commission has already been paid with the transfer, large commissions have been filmed every year.

How to bargain? As an everywhere. Call other pension companies to find out where more favorable conditions are ready to offer. Go to your current insurance agent and say: "Izya, and you know that Shmulik suggested that I have the conditions twice better than you suggested?" If the insurance agent is spoiling and: "Wait, a brother, not boiling, here you have percentages twice below, see what cake I baked to your visit, I'm sorry, I was wrong," that's all good. If the insurance agent will be a bad man or a radister in general, you need to be ready to leave courageously.

Lifehak. In 2016, the situation happened from the category "there would be no happiness, but misfortune helped." The fact is that the Ministry of Finance loves Israel's citizens. Of course, first of all, it loves himself greatly, but it happened that it is hard to love yourself, not love others. There really do not want the people to walk in Bituah Leumi. So much that every time someone comes there, somewhere in Israel, the employee of the Ministry of Finance is crying. Therefore, they announced the competition between pension companies for the provision of minimum commissions for pension deductions and accumulation. The tender was won by two companies: Alman Aldobi and Meytav Dash.

Both companies have pledged to provide minimal commissions in the market for the next 10 years. It turned out they do this due to the fact that they do not work with agents, but communicate with customers directly. Therefore, it makes sense to think about the transition for the next 10 years to them, but (!) Be sure to consult with proven pension consultants before taking such actions.

Yet lifehak. In the tablet, the bottom line touched the insurance. Of course, money is also paid for these insurance. And here it is worth approaching it with the mind. If you are a single, and no one depends on you, then why do you need life insurance for example? Who is your heir? If you do not have a wife and pineapples, then why the insurance for his wife and pineapples? If the company considers disability as 75%, then why is the disability insurance, if it gives Leumi bitahs? All this should be clarified in a conversation with a pension company or with a pension agent and get rid of or on the contrary add the necessary insurance.

Maslulum

This is an important term in understanding how a pension is formed in Israel. Let's start with what we will ask the question that happens to those money that we will deduct from our salary. They do not dig in a large safe under reliable protection. Instead, they fall into no less large stock market boiler. And start working there.

If you know what stock market is, it immediately comes an alarming understanding that our money is not particularly protected. That is, it hung the crisis, the stock exchanges got in the refrigerator instead of red fish cheap sausages. By the way, it happened in 2008, when the very crisis happened. People who came out in that year retired, was not very lucky.

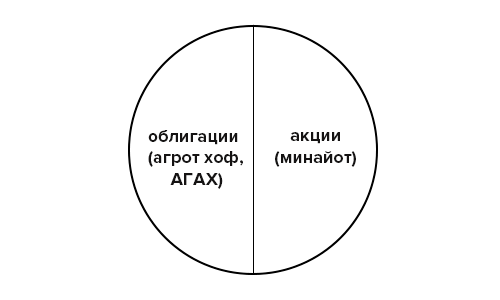

And then the very term comes to the scene - maslul(In the plural - Maslyulim).

Maslyul is, if you can put it, the route in which money falls on the most stock markets. The stock market is very rude and simplified can be represented as in the picture below.

He, the market consists of bonds and shares. Bonds in Hebrew are called "Hof Agram", and the abbreviation of the AGA is often used in speech. Bonds are debt obligations. For example, the state of Israel urgently needs money to upset the underground wall of peace-loving themselves know from his Zionist aggression. The state goes to the United States or to its inhabitants, asks to give money, and in return gives bonds. Every year on these bonds promises to pay the percentage, and after some kind of years, the amount claimed to be debt. Their liquidity in the markets is low, the percentage of them is small, so they are considered a solid tool.

Shares are also securities. They give the right to the owner to participate in the management of the company that these shares released. When you buy one share Apple or "Falaphle Yoshi", you become co-owner. You can even receive dividends (part of profits). The liquidity of shares is high and large and risks. For example, when the cult third iPhone came out, Apple shares fabulously rose. When Shmulik discovered the falapho in front of the "Falaphle of Yoshi" and to Falafel began to offer free pit and scratching the ear, Yosie shares fell in price. This is a risky tool.

And that is the most Maslyul determines what exactly the proportion of retirement money falls on the stock market. Very safe - this is 100% money to throw in bonds. Very risk - 100% of money to throw in stock. Those or other proportions in the middle - just what you need to follow and what to fit with the mind.

If we worked with you - and very often it happens that we worked, then the money falls into Maslyul clay: up to 70% - bonds and up to 30% - stocks.

If at the same time we are 50 years old, then everything is not so bad. Prior to a pension for more than 10 years, these 30% of the shares are a risk that can afford. If we are 67, and in the yard of 2008, then with a high probability, we remain without 30% of money and instead of snacks for lunch suck.

The state took care of such slapping people (well, so that we do not decide to put in Bituah Leuma for the benefit of the subsistence minimum), and adopted the Chilean system. It is that the increasingly to the retirement age, the more solid becomes Maslyul - less shares, more bonds.

But if you are responsible, then you have all the tools in your hands to decide how your money will work. If you take the same crisis of 2008, now in 2017 no one will remember. Exchange grew, the situation has improved. Therefore, knowing that before retirement you still 40, it is quite possible to afford the maximum risk (maximum actions, minimum of bonds) for the nearest, say, 10 years. This will bring maximum interest from the money exchange. After 10 years, the risk can be reduced by choosing a little less risky maslul, and so, approaching the pension, gradually increase the share of solid tools in its "portfolio" and reduce the proportion of risky.

You can go even further. If you really understand how the stock market works, you have the necessary experience, instruments and knowledge, you can come to the pension company and declare: "I can't cope with no snotty." We subscribe the necessary paper and get your retirement money at your full order with the ability to decide where to invest.

Personally, I do not understand anything in this, therefore, such an acrobatics can be preferred. By the way, usually pension companies do not buy any specific shares. Rather, indexes are bought. For example, the Tel Aviv35 index. This is a certain averaged index of 35 of the largest companies in Israel, in which these companies are somewise balanced. One company has grown stocks - the index has grown up, another company has fallen stocks - the index decreased, several companies have grown and fell shares - the index has changed to a certain delta.

So I understand it very simplistic. If in the commentators there will be people with deep knowledge in this area, and the actual errors will cut your eyes, correct me.

At this stage, we must forever disappear the stereotype that we are not managed and do not affect our pensions. In Israel, it is possible to make the most influence on its savings and their size. And at the same stage, an understanding should appear that the responsibility and self-organization is needed in order to control what is happening with our deductions with certain periodicity.

Another lifehakuntil I forgot. On Facebooks always ask if you have Pitsuim, and if there is, you must advise them to take. So, if you return higher on the article, we see that Pissum is actually a third pension. It is not necessary to take them without extreme need. Just because you should not deprive yourself a third of your pension.

And notice. Since for his life, a person, as a rule, changes not one thing, not two, and not three, then such a phenomenon is very common, as "dependent" somewhere in retirement money. Well, and if somewhere lost something, there will always be good guys who will help you find it. According to the same Facebook, stories often walk, as some people turned to someone and said that they would find lost retirement money. They asked to sign the contract, which will be paid from the found, say 30%. Not really thinking, a person signs, and when he "finds" the 200,000 shekels, he is terrified by the fact that with his money you need to give a third.

After all, the money was not really lost and you can get all the information about pension savings on the public website Swiftness.co.il. It costs 40 shekels. In addition, there is a website where you can find your funds with non-working savings. Just people often do not know about it, or they are lynching and afraid to understand. In fact, even the pension consultant will take all the data about you from the first site, everything will tell and give advice, but not for a third of the money "found", and for some hourly rate.

Pension report

Once a quarter and at the end of the year we receive reports on our pension affairs from pension companies. Below I will attach an exemplary photo of how they look. If the article picks up 50 shores on Facebook, in other words, it will be really useful and interesting people, I will supplement this pension report with explanations that we see on it. By the way, it is noticeable that Dmy Nouli Wild. This is because the type of pensions - Bituah Menaelim.

How to open pension baskets

First, by law, no one has the right to impose you some kind of pension company and the type of pension deductions. If you carelessly wave a paw, the employer will call you the agent of the pension company with which it works. You will all open, sign and, most likely, will neatly begin to lick the highest percentage of commissions permitted by law.

But you have the right to poke your finger into a particular company and say that you are interested in Keren pension or it is Capat Gemel. And no one has the right to object.

You are also entitled to specify a specific insurance agent with which you want to work, and not an employer.

Secondly, if you had no pension program before, and this is your first job, you will open all this thing to you six months after the start of work. After the discovery of the deduction over the past six months will occur retroactively. That is, as a result, these six months will not remain without pension deductions.

At each next place of work, the pension program opens minimum 3 months after the start of workand similarly retroactively.

Here, too, you need to be attentive because they may not ask and write off all the pension deductions for the past (six months in the first case) three months with a salary. If the salary is small, and you were to this black, it can hit the budget for a month, fresh galley instead of a juicy steak and so on. But everyone can be divided into payments, manifesting in advance vigilance.

conclusions

Here, in fact, everything that I could remember on this topic. All of the above pursues on the following conclusions: Pension in Israel causes a person to be responsible. If you put everything on a samone, then "you can finish", as they say. We have to bargain for commissions, decide whether to risk whether and earning great interest or not risking, and earn small interest. This is a personal decision of everyone. We need to remember that Pissuim is part of our pensions that pension programs are not open immediately, and that it is necessary to check pension deductions in the same way as we check the bank account for the salary at the beginning of the month.

Well, of course, ideally, you need to have your own cube on old age, because pensions with pensions, programs programs, and I will never take care of yourself.

If the article had gross mistakes, I am very welcome to design comments and corrections, preferably with reference to the letter of the law. I study with you.

In order for you to read this article for free, I paid for the seminar and spent a lot of time in order to recycle information in a simple and understandable form. Therefore, below the address where you can send a "cup of coffee" and support the project. This will help its development and content. And as always, Like, Cher, repost; Subscribe to